The American Hospital Association estimates the lost revenue to hospitals from the pandemic to be $50.7 bil. per month or $202.6 bil. over the four-month period March 1 through June 30, 2020. Their estimates are based upon expected cancellations of patient services, increased costs of personal protective equipment, and increased expenses tied to providing support to frontline workers.

To survive, provider organizations must quickly restore their previous revenue streams while preparing for the potential next waves of the pandemic. Successful recovery for these organizations is not represented by a return to the old ways of providing services. The road to recovery requires phased responses to the challenges that lie ahead. Service lines and supporting processes must evolve to create a more nimble and responsive organization that delivers better outcomes and enhanced patient experiences.

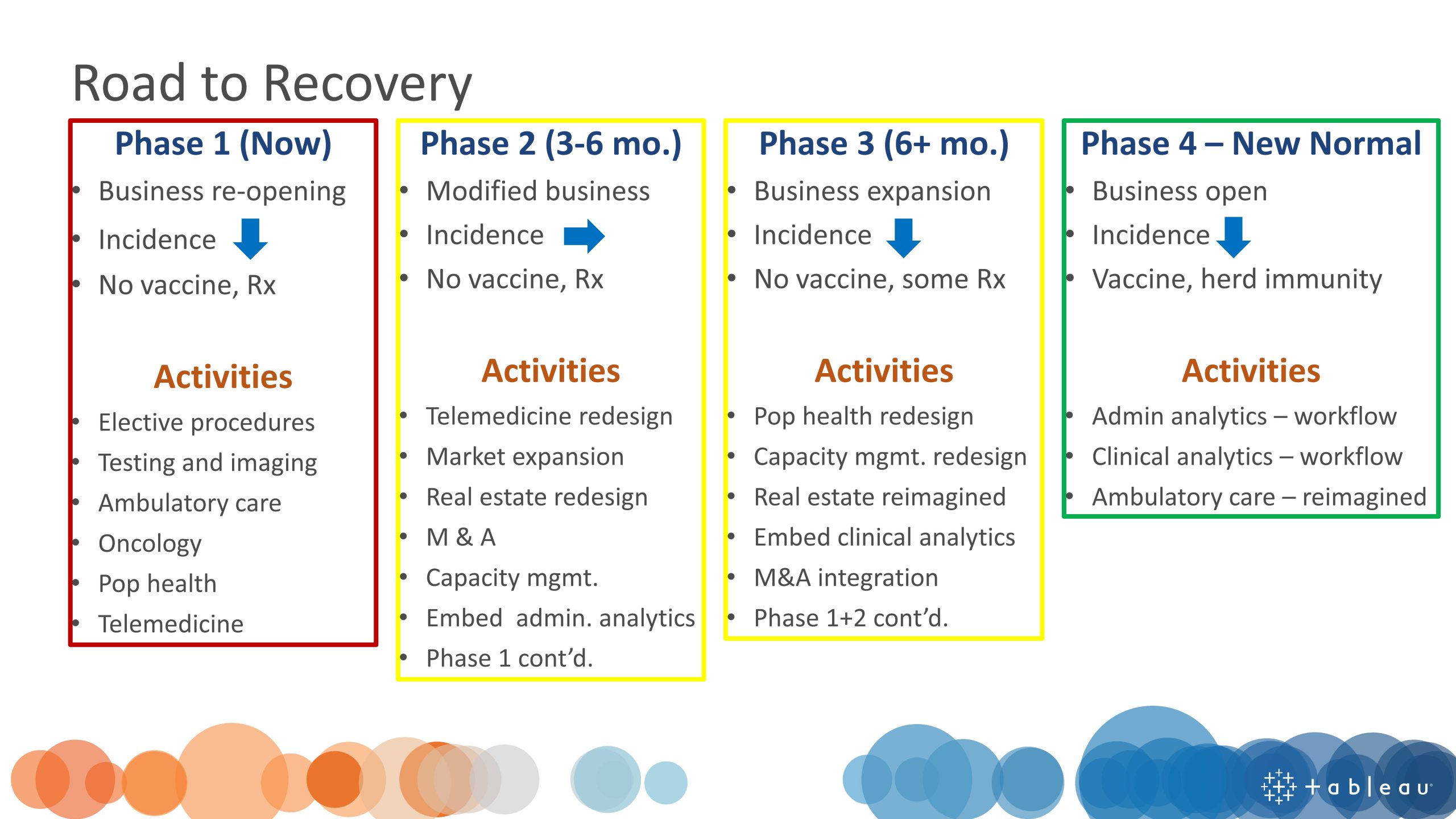

The four phases of the road to recovery for provider organizations are described as:

Phase 1 (Now) – businesses reopen and decreasing COVID-19 incidence rates with no vaccine or effective treatments available.

Phase 2 (3-6 months from now) – businesses modified to manage viral spread, stable COVID-19 incidence rates with no vaccine or effective treatments available.

Phase 3 (6+ months from now) – businesses expand services and decreasing COVID-19 incidence rates with no vaccine or effective treatments available.

Phase 4 (New Normal) – businesses fully open and incidence of new infections stable with a vaccine or protective herd immunity available.

During Phase 1 of recovery, provider organizations will focus on the following broad areas: elective procedures and surgeries, diagnostic imaging, oncology, population health, ambulatory care, and telemedicine to begin to revive revenue streams.

While these areas broadly identify what offerings might help recover revenue, each organization must examine in detail all available service line capabilities. They then must prioritize the service lines that deliver the greatest revenue while simultaneously maximizing the efficient use of available facilities and staff. In addition, all restart plans must anticipate future waves of COVID-19 cases and provide for any potential curtailing of services.

Although meaningful cost accounting of service lines is hard to come by for most organizations, analysis of historical trends offers some valuable insight into what services may prove most profitable. Insightful dashboards can be built to reveal previous treatment trends by service line and month of service. Using these trends as a baseline, organizations can prioritize which service lines to restart and track their restart progress by comparing current utilization to these historical trends.

Each service line can be broken down into intertwined processes with productivity dashboards created to manage each process. In addition, other dashboards tracking the entire service line can inform both managers and front-line staff as they work to ramp up capacity.

How will this work? Let us take elective knee replacement surgery as an example. First, the patients needing surgery, including those who had their surgery cancelled due to the pandemic response and other patients who planned to schedule their surgery, need to be identified. Hospital EMRs should be able to identify these patients. Next, available resources must be inventoried (e.g., operating theater time blocks). Again, the EMR and existing ERP systems should be able to provide this data. Last, organizations must then contact the list of targeted patients to reschedule them for surgery. This can be accomplished using CRM software or similar capability built into the EMR. And to make it all work efficiently, this process must fit within an established workflow that maximizes the use of facilities and staff.

In Part 2 of this four-part Provider Road to Recovery series, I will describe new opportunities to secure lost revenue that will be presented once the pandemic moves into Phase 2.